Posted by Jake on Sunday, July 03, 2011 with 11 comments | Labels: Article, banks, benefits, Big Society, budget cuts, inequality, jobs, pay, pensions

According to the Department of Works and Pensions, the official poverty line for pensioners with no dependent children is

Single Person: £166 per week

Couple: £248 per week

According to the Hutton report on public sector pensions, the median pension (i.e. the amount that half the people in the group get less than) for Local Government workers and for NHS staff places them in poverty. This is even after receiving the State Pension on top of their ‘gold plated’ occupational pensions.

That puts 790,000 Local Government and NHS pensioners in poverty. The Hutton report also shows that a further 750,000 public sector pensioners are no more than £50 a week above the poverty line.

The government is trying to take money from hundreds of thousands of Britons who are in or near poverty, to fix the crisis caused by bankers who are rolling in it. Why are MPs so heartless? As public servants, do they not feel the same pain from these severe public sector pension downgrades?

Actually, they don’t. For two main reasons

a) Their own magnificently subsidised pensions

b) Their remunerated hobbies

MPs' Pensions

MPs have three options for growing their pensions. They can get...

One-fortieth of their final salary for each year of service, by contributing 11.9% of their salary

One-fiftieth of their final salary for each year of service, by contributing 7.9% of their salary

One-sixtieth of their final salary for each year of service, by contributing 5.9% of their salary

Overall, as a herd, MPs contribute a little under 10% of their salaries.

At current salaries, using the “1 fortieth” rate, an MP adds £1,643 per year to his pension for each year he works as an MP, equivalent to £137 per year to his pension for each month he works.

So, at this rate of growth, how long does it take an MP to build up a pension equal to the average (median) pension of various public sector workers? (PCPF=Parliamentary Contributory Pension Fund)

Local government worker: £3,048 2 years 3 months

NHS worker: £4,087 3 years 6 months

Civil Servant: £5,023 4 years 1 month

So in less than the life of one single Parliament the MPs would be better off than one million public sector pensioners, from whom they intend to take money.

“According to evidence from the Government Actuary’s Department (GAD), the mean length of service (excluding transfers in and added years) of active PCPF members at the time of the latest valuation in 2008 was 12.2 years, while the mean length of service (again excluding transfers and added years) of those who left at the election in 2005 was 14.4 years.”

With 14.4 years service an MP could build up a pension worth £23,500 per annum at current salary figures. This pension is index linked to RPI, and provides five eighths of the amount to the widowed spouse after the MPs death. According to the FSA’s moneymadeclear.org.uk website, you would need a fund of about £700,000 to buy this annuity from the likes of Aviva, Legal & General, and the Prudential insurance companies.

MPs remunerated hobbies

MPs don’t have to rely on their parliamentary pensions. MPs claim that their jobs are so very demanding, using this as a reason to push up their pay and perks, and a justification for pinching expense money. And yet these same MPs find time for other jobs.

The Members' Register of Interests show MPs find time for other well remunerated activities. Let's randomly look at MPs whose surnames begin with "M":

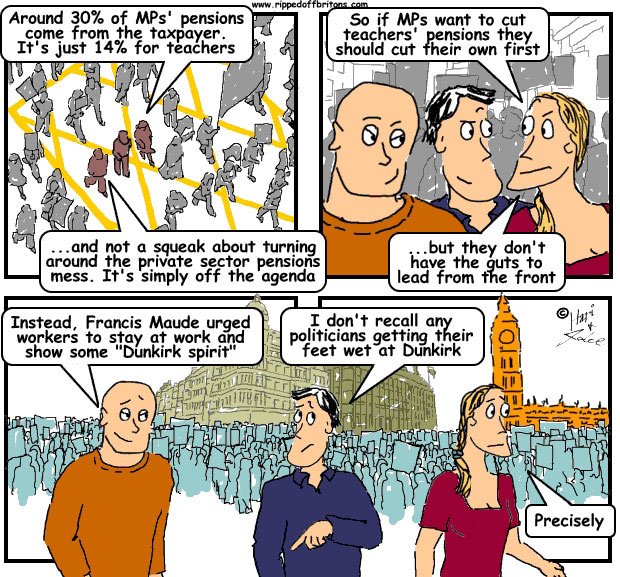

Francis Maude: (currently pushing through the public sector pension cuts)

was paid £9,203.23 for 15 hours work on a Barclays Bank advisory board.

Alan Milburn: (Former member for Darlington, and former Health Secretary)

Member of Lloydspharmacy's Healthcare Advisory Panel. (£25,001-£30,000) Remuneration paid annually.

Member of European Advisory Board of Bridgepoint Capital Limited. (£30,001-£35,000) Remuneration paid annually.

Member of the Advisory Board of PepsiCo UK. (£20,001-£25,000) Remuneration paid annually.

Andrew Mitchell: (Sutton Coldfield)

Paid £14,375 (inclusive of VAT) for 24 hours work as Supervisory Board member.

Paid £10,350 (inclusive of VAT), for 10 hours for management consultancy work

In 2010 three MPs, Geoff Hoon, Stephen Byers, and Richard Caborn, were caught out peddling influence by the Channel 4 “Dispatches” programme. Byers commented “I am a bit like a cab for hire”. The daily rate of £5,000 per day seems to be pretty consistent, whether advising a bank or being a cab for hire.

In a day an MP can earn more than the annual pension of 1 million public sector workers. Cutting public sector pensions? A politician will grasp at any straw so long as it is someone else drowning.

A few years ago, during the last Labour government, another Lord reviewed pensions. Lord Turner came up with proposals with many similarities to those of Lord Hutton. Broadly speaking, there is not much practical difference between the intentions of the Labour and the Conservative leadership.

Not only did Lord Turner make recommendations on pensions, including pushing up the retirement age, he also spoke frequently about the Financials Services industry and the City:

“I suggested that some of the activities which went on in the trading rooms of some banks in the run up to the financial crisis were ‘socially useless’. People have asked me whether I regret those comments. The answer is no, except in one very small respect. Which is that I think it would have been better to use the phrase ‘economically useless’”

So why is the government so determined to take money from the poor, and ignore this handsome stash of guilty cash? After all, the City is the central player responsible for our current financial crisis. The excessive costs for financial services – including the pillaging of pensions by high charges – drain our money futilely (no link between pay and performance) into excessive pay for bankers? The £2.5 billion bank levy is small beer put next to the amounts paid in bonuses. There is a lot more where that came from.

As Mervyn King, governor of the Bank of England, stated:

One would hope that public sector pensioners also have something tucked away from other periods of employment. Not that many clock up 40 odd years with the same employer. If they did then they should be on at least half pay at retirement. The median pensions level is low because it includes many with short service.

ReplyDeleteBull pizzle. Median pensions are low because a lot of public sector workers are on low pay in the first place. Many office grade staff stay in low-paid jobs for the long haul. I worked in the water industry for all of my working life (37 years) and a good proportion of the office staff had 30 years service or more.

DeletePensionsManager, I'd love to do the maths on that. Your comment prompted me to do a bit more digging. Can you recommend any data sources? The best source I could find for local government workers is - http://www.lga.gov.uk/lga/core/page.do?pageId=7419778

ReplyDeleteBasic data from here suggests:

a) 490,000 FTE (Full Time Equivalent) staff earn less than £17,802 per annum

b) Accrual rate upto 2008 was one eightieth.

c) Accrual rate since 2008 is one sixtieth.

From this, for someone retiring today, on a final salary of £17,802, to get the median local government pension of £3,048 would take a bit over 12 years.

It would have taken 21 years of service for this person to get a pension of £5,000 per annum.

And that's on a "final salary" basis. "Career average", which is the current proposal, would take a sizeable bite out of this.

After the March2012 Austerity Budget, Daily Mail reports "Maude and his Cabinet friends give their gold-plated pensions a boost as they push through reforms"

ReplyDeletehttp://www.dailymail.co.uk/news/article-2124291/Maude-Cabinet-friends-gold-plated-pensions-boost-push-reforms.html#ixzz1qzK71Y9n

What i cant understand is that given the current pensions issues and the high news coverage over them, why do we not see any shouts about politicians pensions in the news, surely this would highlight the complete double standards that are going on between the goverment and the hard working people of great britain.As you say,if their going to cut them then they should start with their own. No chance of that i guess.

ReplyDeleteWhy do we not see this in the media? Simples, the BBC say exactly what the Tories tell them to say! They all used to towel flick each other in the Eton boys shower!

DeleteFinal Salary pensions for MP's should end on the date of the next election. This crop ought to be the last to benefit from this scheme.

ReplyDeleteThe next crop of MP's should be auto-enrolled into NEST because "we're all in it together" and the only way to be in it together is to experience it together.

I think that Defined Contribution Schemes and NEST would suddenly become the MOST IMPORTANT thing on the Parliamentary agenda. QE would end immediately, the EU gender directive would be kicked so far into the long grass it would never be seen again and we'd definitely see pension funds going back to being TAX FREE.

The only way to get an MP's attention is to attack his wallet.

Telegraph reports: "MPs will escape George Osborne’s pensions tax raid

ReplyDeleteMPs will not be affected by George Osborne’s latest tax raid on pensions, even though private sector workers with identical retirement incomes will be hit, said experts."

http://www.telegraph.co.uk/news/politics/9733500/MPs-will-escape-George-Osbornes-pensions-tax-raid.html

The reason we don't see this in the media is because the government controls the media.simples!

ReplyDeleteI think unless bankers & MP's are brought to case regarding these matters there will never be any fairness as they have nothing to fear. We put them there (although not this lot) & we should have the power to kick them out regardless of how long they've been there.

ReplyDeleteParliamentary Report states that based on the proposed new pension rules for the Fire Brigade, if a fire-fighter retires early at the age of 55 due to not meeting the 'fitness requirements' his pension will be reduced by 47% from £17,151 to £9,073. The same report also states that 85% of Britons at 55 years of age would not meet the 'fitness requirements'.

ReplyDeletehttp://www.parliament.uk/briefing-papers/SN06585/firefighters-pension-schemes-current-reforms

A document produced by the Fire Brigades Union in November 2013 states that out of 40,722 employees just 563 were over 55.

http://img.fbu.org.uk/wp-content/uploads/2013/11/Consultation-on-fitness-and-capability-_submission-final_.pdf